Jewelry Insurance Policies: Your Complete 2026 Guide

Posted by AOD on 7th Jul 2026

Jewelry Insurance Policies: Your Complete 2026 Guide

TL;DR:

- Jewelry insurance provides broader, worldwide protection against theft, damage, and mysterious disappearance. Standard homeowners policies often limit coverage and exclude key risks, making dedicated policies essential for valuable pieces. Proper appraisals and choosing the right coverage structure ensure accurate protection and smooth claim processes.

Jewelry insurance policies are specialized coverage plans designed to protect your valuable pieces against loss, theft, accidental damage, and mysterious disappearance. Standard homeowners or renters insurance rarely provides adequate protection. Most policies cap jewelry theft coverage at just $1,000 to $2,500, leaving collectors and luxury buyers dangerously exposed. Dedicated jewelry coverage fills that gap with worldwide protection, broader perils, and tailored deductible options. Keeping a current appraisal, updated every 2–3 years, is the foundation of any sound coverage plan.

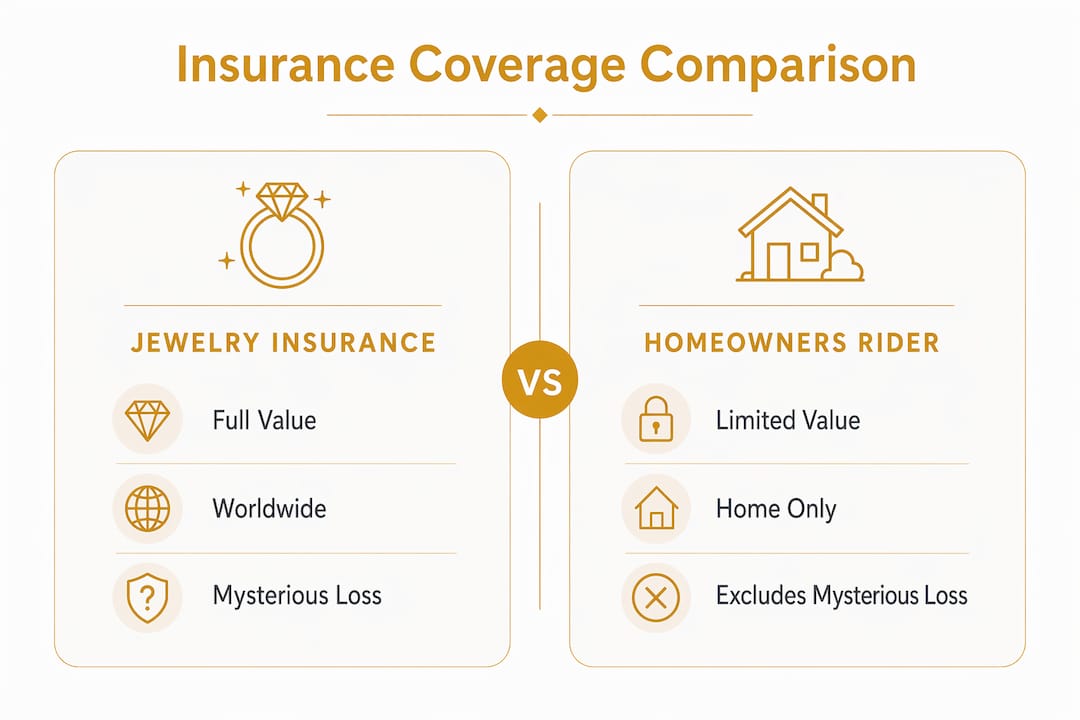

What do jewelry insurance policies actually cover?

Dedicated jewelry insurance policies cover a far wider range of perils than any standard homeowners rider. A standalone policy typically protects against theft, accidental damage, stone loss, and mysterious disappearance. That last category matters more than most people realize. Losing a ring without any evidence of theft is one of the most common real-world losses, and standard policies exclude it entirely.

Coverage also extends worldwide. Whether your opal pendant goes missing in a hotel room in Paris or your diamond ring is damaged on a hiking trail in Colorado, a standalone policy responds. Homeowners insurance, by contrast, typically covers only losses that occur on your property or within narrow geographic limits.

Two coverage structures exist: scheduled and blanket. Scheduled coverage lists each piece individually with its appraised value, providing the most precise protection for high-value items. Blanket coverage sets a single dollar limit across all jewelry, which works for modest collections but leaves gaps when one piece far outweighs the others in value. For a one-of-a-kind opal from Lightning Ridge or a custom-designed piece, scheduled coverage is the right choice.

How much do jewelry insurance policies cost?

Annual premiums typically range from 0.5% to 2% of the jewelry’s appraised value. That means a $10,000 piece costs between $50 and $200 per year to insure. Specialized providers often land in the 0.5%–1.5% range, making dedicated coverage more affordable than most owners expect.

Several factors shape your exact premium. Location plays a role because theft rates vary by region. The type of coverage selected, all-risk versus named peril, also affects cost. All-risk policies cover every cause of loss except those explicitly excluded. Named peril policies only cover the specific events listed, such as fire or theft, and tend to cost less but leave more gaps.

Deductible choices have a direct impact on your premium. A higher deductible lowers your annual cost but increases what you pay out of pocket when you file a claim. For a piece you wear daily, a low or zero deductible often makes more financial sense.

| Appraised value | At 0.5% annually | At 1% annually | At 2% annually |

|---|---|---|---|

| $2,500 | $12.50 | $25 | $50 |

| $5,000 | $25 | $50 | $100 |

| $10,000 | $50 | $100 | $200 |

| $25,000 | $125 | $250 | $500 |

Pro Tip: Request itemized quotes from multiple providers and compare deductibles, coverage limits, and exclusions side by side. Price alone tells you very little about the actual protection you are buying.

Jewelry insurance vs. homeowners insurance: what’s the real difference?

The coverage gap between dedicated jewelry insurance and a standard homeowners rider is significant. Understanding it protects you from a painful surprise at claim time.

| Feature | Dedicated jewelry insurance | Homeowners rider |

|---|---|---|

| Theft coverage | Full appraised value | Sub-limit: $1,000–$2,500 |

| Mysterious disappearance | Included | Usually excluded |

| Accidental damage | Included | Rarely included |

| Worldwide coverage | Standard | Limited or excluded |

| Impact on home policy | None | May raise premiums or cause non-renewal |

| Deductible options | Flexible, including zero | Tied to home policy deductible |

Filing a jewelry claim on a homeowners policy can increase your home insurance premiums or even trigger non-renewal. That risk disappears with a standalone policy. Jewelry claims on dedicated policies stay entirely separate from your home coverage.

Standalone jewelry insurance also tends to include coverage for new purchases, giving you a short window after buying a piece before you need to formally add it to your policy. Some policies even cover preventive maintenance costs, such as prong retipping, which reduces the chance of stone loss.

Pro Tip: If you own any piece worth more than $2,500, a standalone policy almost always makes more financial sense than relying on a homeowners rider. The premium difference is small. The coverage difference is enormous.

Why are professional appraisals critical for insuring jewelry?

A professional jewelry appraisal is a legal document, not just an estimate. It describes every measurable characteristic of a piece in enough detail that another jeweler could recreate it without ever seeing the original. That level of documentation is what insurers require to pay a claim accurately.

Receipts and gemstone certifications are not substitutes. A purchase receipt proves what you paid, not what the piece is worth today. A gemstone certificate describes the stone but does not account for the setting, craftsmanship, or current market value. Only a formal appraisal written by a certified professional establishes the replacement value an insurer will honor.

Key facts about appraisals every jewelry owner should know:

- Update frequency: Experts recommend updating appraisals every 2–3 years to reflect current market values. Precious metal and gemstone prices shift meaningfully over time.

- Replacement value basis: Insurance pays out based on current replacement value, not original purchase price. An outdated appraisal is the leading cause of claim disputes.

- Fee structure: Appraisers who charge a percentage of the appraised value create a conflict of interest. Choose appraisers who charge flat fees or hourly rates.

- Certification: Look for appraisers credentialed by recognized bodies such as the American Society of Jewelry Appraisers or the Gemological Institute of America.

- Storage: Keep digital and physical copies of your appraisal in separate secure locations. Your insurer will need it immediately when a claim is filed.

Understanding opal jewelry valuation is particularly important for collectors of rare Australian opals, where play-of-color, origin, and rarity all factor into replacement cost in ways a generic appraisal may undervalue.

Pro Tip: Schedule your appraisal update at the same time each year, perhaps when you renew your policy, so it never slips through the cracks.

How to choose the best jewelry insurance policy for your needs

Selecting the right policy requires more than comparing annual premiums. Work through these steps to find coverage that genuinely fits your life and your collection.

-

Inventory your collection. List every piece you own along with its estimated value. This tells you whether scheduled or blanket coverage makes more sense and gives you a baseline for comparing policy limits.

-

Get current appraisals. No insurer can accurately cover what has not been properly valued. Before requesting quotes, confirm that your appraisals reflect today’s replacement costs.

-

Prioritize all-risk coverage. Named peril policies leave gaps that only become visible at claim time. All-risk policies cover mysterious disappearance, accidental damage, and other losses that named peril policies miss entirely.

-

Evaluate your lifestyle. If you travel frequently or wear your jewelry daily, worldwide coverage and a low deductible are non-negotiable. If pieces stay in a safe most of the time, you may have more flexibility on deductible levels.

-

Assess the claims process. Ask each insurer how claims are settled. Some pay cash; others require replacement through a network jeweler. Cash settlement gives you more freedom to replace a piece with a comparable one from a trusted source.

-

Check the insurer’s reputation. Look for independent ratings and customer reviews focused specifically on claims handling. A low premium means nothing if the insurer disputes claims routinely.

-

Read the exclusions carefully. Every policy has them. Common exclusions include wear and tear, intentional damage, and losses during certain activities. Know exactly what your policy will not cover before you sign.

Reviewing questions to ask before buying gemstones can also prepare you to ask equally sharp questions of your insurer. The same diligence that protects you at purchase protects you at claim time.

Key Takeaways

Dedicated jewelry insurance policies provide protection that standard homeowners insurance cannot match, making standalone coverage the right choice for any piece worth more than $2,500.

| Point | Details |

|---|---|

| Standard coverage falls short | Homeowners policies cap jewelry theft at $1,000–$2,500 and exclude mysterious disappearance. |

| Annual cost is modest | Premiums typically range from 0.5% to 2% of appraised value, often $50–$200 per year for a $10,000 piece. |

| Appraisals drive claim outcomes | Current, professionally written appraisals based on replacement value prevent disputes and underpayment. |

| Standalone policies protect home coverage | Jewelry claims on dedicated policies do not affect homeowners premiums or renewal status. |

| Policy details matter more than price | Coverage for mysterious disappearance, worldwide protection, and deductible flexibility separate strong policies from weak ones. |

Why I always recommend going standalone from day one

People consistently underestimate how much their jewelry is worth until something goes wrong. I have seen collectors with pieces valued at $15,000 or more still relying on a homeowners rider with a $1,500 sub-limit. They assumed their policy was adequate because they had never read it carefully. That assumption is expensive.

The mysterious disappearance exclusion is the one that catches people off guard most often. A ring slips off during a beach vacation. A pendant clasp fails somewhere between the hotel and the restaurant. There is no theft to report, no accident to document. Without all-risk coverage, that claim is denied. Full stop.

I also feel strongly about zero-deductible or very low-deductible policies for pieces you wear regularly. The stress of a loss is already significant. Adding a $500 or $1,000 out-of-pocket cost on top of it makes the experience worse and sometimes discourages people from filing at all.

The appraisal conflict-of-interest issue is real and underappreciated. An appraiser paid a percentage of the value they assign has a financial incentive to inflate that value. That sounds like it benefits you, but it creates documentation that insurers can challenge. A flat-fee appraiser has no stake in the number and produces a document that holds up. Always ask how your appraiser charges before the appointment.

For rare pieces, particularly custom or one-of-a-kind opals with irreplaceable play-of-color, I recommend reviewing opal insurance coverage specifics before selecting a policy. Generic jewelry policies sometimes undervalue gemstones with unique characteristics that a standard replacement cannot replicate.

— Renee

Protecting the pieces that matter most

Every piece of fine jewelry carries more than monetary value. It holds memory, artistry, and in the case of rare Australian opals, a fragment of the earth’s own kaleidoscopic light. Protecting that investment with the right coverage is an act of respect for what you own.

Australianopaldirect specializes in authentic, ethically sourced opals from Lightning Ridge, Coober Pedy, and Queensland, each piece accompanied by the documentation and transparency that makes proper insurance coverage straightforward. When you know exactly what you own and what it is worth, insuring it becomes simple. Visit Australianopaldirect to explore the collection and learn more about protecting your most luminous investments. The role of insurance in a jewelry purchase is something every buyer deserves to understand before they fall in love with a piece.

FAQ

What do jewelry insurance policies typically cost?

Annual premiums range from 0.5% to 2% of the piece’s appraised value. A $10,000 piece generally costs between $50 and $200 per year to insure.

Does homeowners insurance cover jewelry loss?

Standard homeowners policies cover jewelry theft only up to a sub-limit of $1,000–$2,500 and typically exclude mysterious disappearance. Scheduling a piece or buying a standalone policy provides full protection.

How often should I update my jewelry appraisal?

Appraisals should be updated every 2–3 years to reflect current replacement costs. Precious metal and gemstone prices shift enough over time to create significant gaps in coverage if appraisals go stale.

What is mysterious disappearance coverage?

Mysterious disappearance covers loss of a piece when there is no evidence of theft or a specific accident. Standard homeowners policies exclude this peril; dedicated jewelry policies include it as standard.

Can I insure custom or one-of-a-kind jewelry pieces?

Yes. Scheduled coverage on a standalone policy is specifically designed for unique pieces. A detailed professional appraisal that documents the piece’s characteristics fully is required to establish the correct replacement value for claims.