The Role of Insurance in a Jewelry Purchase

Posted by AOD on 1st Jul 2026

The Role of Insurance in a Jewelry Purchase

TL;DR:

- Jewelry insurance offers specialized coverage that protects against theft, loss, and mysterious disappearance from the moment you acquire a piece. It is the most effective way to safeguard your investment and is essential immediately after purchase to prevent financial loss. Most buyers underestimate the importance of a standalone policy and timely appraisals, risking underinsurance and higher premiums.

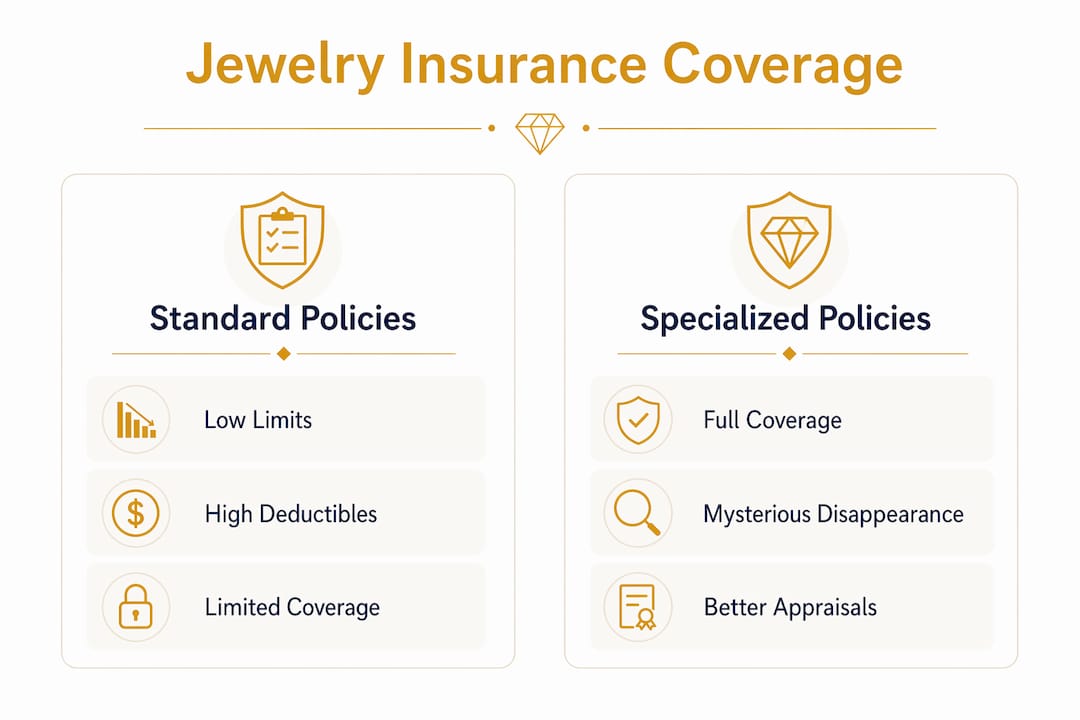

Jewelry insurance is defined as specialized coverage that protects your pieces against theft, loss, accidental damage, stone loss, and mysterious disappearance, offering financial security that standard homeowners or renters policies rarely match. The role of insurance in a jewelry purchase goes far beyond paperwork. It is the difference between recovering the full value of a treasured piece and absorbing a loss that no amount of sentiment can offset. Whether you have just acquired a Lightning Ridge black opal or a diamond engagement ring, the moment that piece leaves the store, your financial exposure begins. Understanding your coverage options from day one is not optional. It is the foundation of responsible ownership.

What does jewelry insurance typically cover and how does it work?

Specialized jewelry insurance covers all risks worldwide, including theft, loss, accidental damage, stone loss, and mysterious disappearance from the moment the policy activates. That last peril matters more than most buyers realize. Mysterious disappearance refers to an item that simply vanishes with no explanation, a scenario that standard homeowners policies almost universally exclude.

A standalone jewelry policy operates on what insurers call an “all risk” basis. Coverage applies globally, which means your opal pendant is protected whether you lose it in Sydney, Paris, or New York. Worldwide coverage is a critical benefit for collectors and travelers who carry their most valued pieces with them.

The claims process follows a clear sequence:

- Appraisal on file: The insurer uses your documented appraisal to establish replacement cost.

- Loss report: You file a claim describing the circumstances of loss or damage.

- Repair or replacement: Policies may offer a cash payout, direct repair, or a replacement piece, sometimes through a jeweler of your choosing.

- Settlement: The insurer settles based on the coverage limit set at policy inception.

The key operational difference between a standalone policy and a rider on a homeowners or renters policy is scope. A rider adds jewelry coverage to an existing policy but inherits that policy’s deductibles, claim reporting rules, and coverage caps. A standalone policy is purpose-built for jewelry, with terms designed around the specific risks gemstones and precious metals face.

Pro Tip: Request a policy that includes mysterious disappearance coverage explicitly in writing. Not all riders include it, and the omission can leave you unprotected in the most common loss scenarios.

Why standard homeowners or renters insurance often falls short

Standard homeowners and renters policies cap jewelry coverage at surprisingly low limits. Loss limits often fall around $1,000–$1,500 per item, with deductibles that can exceed the value of the claim itself. For a modern engagement ring or a rare gemstone piece, that cap is financially inadequate.

The sub-limit problem is compounded by deductible math. If your homeowners policy carries a $1,000 deductible and your jewelry sub-limit is $1,500, a stolen ring worth $3,000 yields a net payout of just $500. That gap is real money, and it surprises buyers who assumed they were covered.

| Coverage feature | Standard homeowners policy | Standalone jewelry policy |

|---|---|---|

| Per-item jewelry limit | $1,000–$2,500 typically | Set by appraisal, no cap |

| Mysterious disappearance | Usually excluded | Included |

| Deductible | $500–$2,500 typically | Often zero |

| Worldwide coverage | Rarely included | Standard |

| Claims impact on home policy | Yes, premium risk | No impact |

There is a second risk that buyers rarely anticipate. Filing a jewelry claim on a homeowners policy can classify you as a high-risk policyholder, triggering premium increases or even non-renewal. Claims on standalone jewelry policies do not appear on industry databases like CLUE, which insurers use to assess home insurance risk. That isolation protects your home insurance record entirely.

Pro Tip: If you own high-value jewelry, treat your homeowners policy as a last resort for jewelry claims. A standalone policy keeps your home insurance record clean and your premiums stable.

How to determine appropriate coverage and cost considerations

The right coverage amount starts with a current, accurate appraisal. Rising precious metal and gemstone prices mean that many owners are underinsured if they rely on appraisals that are several years old. An opal appraised at $2,000 three years ago may cost $3,500 to replace today. The appraisal sets your coverage ceiling, so an outdated one leaves a gap that the insurer will not fill.

Specialized jewelry insurance costs 1%–2% of appraised value annually. For a $5,000 piece, that translates to $50–$100 per year. That figure is modest relative to the replacement cost, particularly for rare gemstones like Australian opals from Coober Pedy or Queensland, where market values can shift significantly with supply.

Key factors that affect your premium include:

- Deductible choice: A zero-deductible policy costs more annually but eliminates out-of-pocket expense at claim time.

- Replacement cost vs. cash value: Replacement cost coverage pays what it costs to replace the item today. Cash value coverage deducts depreciation, which can significantly reduce your payout.

- Scheduled vs. blanket coverage: A scheduled endorsement lists each piece individually with its appraised value. Blanket coverage sets a total limit across all pieces. Scheduled coverage is more precise and generally better for high-value individual items.

- Coverage above appraised value: Some standalone policies offer up to 125% of appraised value, protecting you if replacement costs rise between appraisals.

Review your policy and appraisal every two to three years. Precious metal prices and gemstone valuations shift with market conditions, and your coverage should reflect current replacement costs, not historical ones. Australianopaldirect recommends pairing any significant opal purchase with an insurance appraisal from a certified gemologist to establish an accurate baseline.

Pro Tip: Ask your insurer whether the policy pays replacement cost or actual cash value. The difference can amount to thousands of dollars at claim time.

When and who should insure your jewelry

The best time to insure jewelry is immediately upon purchase or receipt. Risk begins the moment a piece leaves the store, and the period immediately after acquisition, especially during travel home or initial wear, is among the highest-vulnerability windows. Delaying coverage by even a few days creates an unprotected gap that no retroactive policy can close.

Who should hold the policy follows the principle of insurable interest. The person who bears the financial loss if the item is lost or damaged is the person who should insure it. In practice, this is almost always the current possessor. For an engagement ring, that typically means the recipient once the ring is given, though the giver may want interim coverage during the proposal period.

Follow these steps to activate coverage correctly:

- Obtain a written appraisal from a certified gemologist before or immediately after purchase.

- Contact an insurer specializing in jewelry coverage and request a standalone policy or scheduled endorsement.

- Document the piece with high-resolution photographs showing all angles, hallmarks, and any unique characteristics.

- Store documentation securely in a cloud backup or fireproof safe, separate from the jewelry itself.

- Review annually and update the appraisal whenever metal or stone prices shift materially.

Special considerations apply to heirlooms. An inherited piece may carry sentimental value far exceeding its market appraisal. Insurance covers financial loss, not emotional loss. For heirlooms, the appraisal should reflect current replacement cost for a comparable piece, not the original purchase price from decades past. Understanding warranty and protection options alongside insurance gives buyers a complete picture of post-purchase security.

Pro Tip: Photograph your jewelry against a plain white background with a ruler in frame. This gives insurers and gemologists an unambiguous reference for size, color, and condition at the time of coverage.

Key Takeaways

Jewelry insurance is the single most effective financial safeguard a buyer can activate, and it works best when paired with a current appraisal and a standalone policy from the day of purchase.

| Point | Details |

|---|---|

| Insure immediately | Coverage should begin the day you take possession, not days or weeks later. |

| Choose standalone policies | Standalone jewelry insurance isolates claims and protects your home insurance record. |

| Update appraisals regularly | Rising metal and gemstone prices make outdated appraisals a direct path to underinsurance. |

| Understand your perils | Confirm that mysterious disappearance and worldwide coverage are explicitly included in writing. |

| Match coverage to value | Annual premiums of 1%–2% of appraised value are modest protection for high-value pieces. |

Why I think most buyers get jewelry insurance backwards

Most buyers treat insurance as an afterthought, something to sort out after the excitement of the purchase fades. That instinct is understandable, but it is also the most expensive mistake in jewelry ownership. The highest-risk moment for any piece is the first 48 hours after purchase, when documentation is incomplete, habits around storage are not yet formed, and the piece is being shown to everyone.

What I have seen repeatedly is buyers relying on a homeowners rider they have never actually read. They assume it covers everything. Then a ring goes missing on vacation, and they discover the rider excludes mysterious disappearance, applies a $1,500 deductible, and will trigger a premium review on their home policy. That is three separate problems from one unchecked assumption.

The other mistake is treating the original purchase receipt as a substitute for an appraisal. A receipt documents what you paid. An appraisal documents what it would cost to replace the piece today, at current market rates for the metal, the stones, and the craftsmanship. Those numbers diverge quickly, especially for rare gemstones like Australian opals, where market values shift with mining output and global demand.

My honest advice: get the appraisal before you leave the jeweler’s building. Activate a standalone policy within 24 hours. Set a calendar reminder to review both every two years. That three-step habit costs very little and eliminates virtually all of the financial risk that comes with owning something irreplaceable.

— Renee

Protecting your opal investment with Australianopaldirect

Every piece in the Australianopaldirect collection carries the weight of genuine Australian provenance, from the fire-lit depths of Lightning Ridge black opals to the soft, milky brilliance of Coober Pedy whites. These are not mass-produced stones. They are singular expressions of the earth’s artistry, and they deserve protection equal to their rarity.

Australianopaldirect supports buyers with complimentary insurance on purchases, a 90-day warranty, and direct access to gemological documentation that makes the insurance process straightforward. Buyers can explore the full opal jewelry collection and find pieces accompanied by the provenance records and appraisal support that insurers require. For buyers who want to understand the full scope of post-purchase protection, the Australianopaldirect blog covers jewelry care and protection in practical detail.

FAQ

What is jewelry insurance and what does it cover?

Jewelry insurance is specialized coverage that protects against theft, loss, accidental damage, stone loss, and mysterious disappearance. Standalone policies typically provide worldwide coverage with zero deductible, unlike standard homeowners riders.

How much does jewelry insurance cost per year?

Specialized jewelry insurance costs 1%–2% of the appraised value annually. A piece appraised at $5,000 costs approximately $50–$100 per year to insure.

Does homeowners insurance cover jewelry theft or loss?

Standard homeowners policies cover jewelry but cap payouts at $1,000–$2,500 per item and typically exclude mysterious disappearance. Filing a claim can also raise your home insurance premiums.

How often should I update my jewelry appraisal?

Update your appraisal every two to three years, or sooner if precious metal or gemstone prices rise significantly. An outdated appraisal leaves a gap between your coverage limit and the actual replacement cost.

Who should hold the jewelry insurance policy?

The person who bears the financial loss if the item is lost or damaged should hold the policy. For an engagement ring, that is typically the recipient once the ring has been given.

Recommended

- Why Warranty Matters for Jewelry: A Buyer’s Guide - Australian Opal Direct

- Opal Insurance Coverage: Protecting Valuable Gemstones - Australian Opal Direct

- The Role of Jeweler in Design Process Explained - Australian Opal Direct

- Explaining Competitive Jewelry Pricing for Smart Buyers - Australian Opal Direct