Explaining Gemstone Investment Risks: What Collectors Must Know

Posted by AOD on 4th Jun 2026

Explaining Gemstone Investment Risks: What Collectors Must Know

TL;DR:

- Gemstone investment risks include illiquidity, market volatility, misrepresentation, and high ownership costs, making it a complex, long-term asset class. Certification from recognized labs like GIA significantly reduces fraud and enhances liquidity, while provenance, rarity, and proper care also influence resale value. Success hinges on patience, disciplined ownership, and thorough due diligence, rather than short-term market timing or enthusiasm.

Gemstone investment risk is defined as the probability of financial loss arising from illiquidity, market volatility, misrepresentation, and high ownership costs that distinguish colored stones from conventional financial assets. Explaining gemstone investment risks clearly matters because the gemstone market operates without the standardized pricing, exchange infrastructure, or regulatory oversight that governs stocks and bonds. Investors drawn to rubies, sapphires, emeralds, and Australian opals from Lightning Ridge or Coober Pedy encounter a category where beauty and rarity coexist with genuine financial complexity. This guide maps every major risk category, from certification gaps to forced-sale discounts, so you can make purchasing decisions with clear eyes and calibrated expectations.

What are the main types of risks in gemstone investments?

Gemstone investment risks fall into four distinct categories, each capable of eroding returns independently or in combination. Understanding all four before committing capital is the foundation of sound gemstone portfolio management.

Illiquidity and market volatility represent the most structurally significant risks. Unlike equities or ETFs, gemstone markets are illiquid with high transaction costs, and demand contracts sharply during economic downturns. Auction houses like Christie’s and Sotheby’s hold major colored stone sales only a few times per year, meaning a seller who needs to exit quickly faces a thin buyer pool and compressed prices.

Fraud and mischaracterization constitute a second, equally serious threat. Sellers may market synthetic or treated stones as natural without laboratory certification to verify the claim. A synthetic ruby grown in a Verneuil furnace can be visually indistinguishable from a Burmese natural ruby worth fifty times more, and without a report from the Gemological Institute of America (GIA) or a comparable authority, the buyer has no reliable defense.

Ownership costs are the silent return killer that most first-time investors underestimate. Storage, insurance, restoration, and transaction costs erode real performance of luxury assets including gemstones. A stone held in a bank safe deposit box, insured at replacement value, and periodically re-polished accumulates costs that compound against any capital appreciation.

Price dispersion and fashion cycles complete the risk picture. Supply shocks, producer concentration, and fashion cycles drive gemstone market volatility, producing heterogeneous returns across stone types. Alexandrite and Paraiba tourmaline have delivered strong collector premiums over the past decade, while many commercial-grade colored stones have stagnated or declined in real terms.

- Illiquidity: exit timelines measured in months or years, not days

- Fraud risk: synthetic and treated stones require lab verification to detect

- Ownership costs: insurance, storage, and certification fees reduce net returns

- Price dispersion: returns vary widely by stone type, origin, and market cycle

- Fashion cycles: collector demand for specific stones rises and falls unpredictably

Pro Tip: Before purchasing any colored gemstone as an investment, request a current lab report from GIA, the American Gem Society (AGS), or the International Gemological Institute (IGI). A stone without one is priced on trust alone.

How does certification affect investment risk and liquidity?

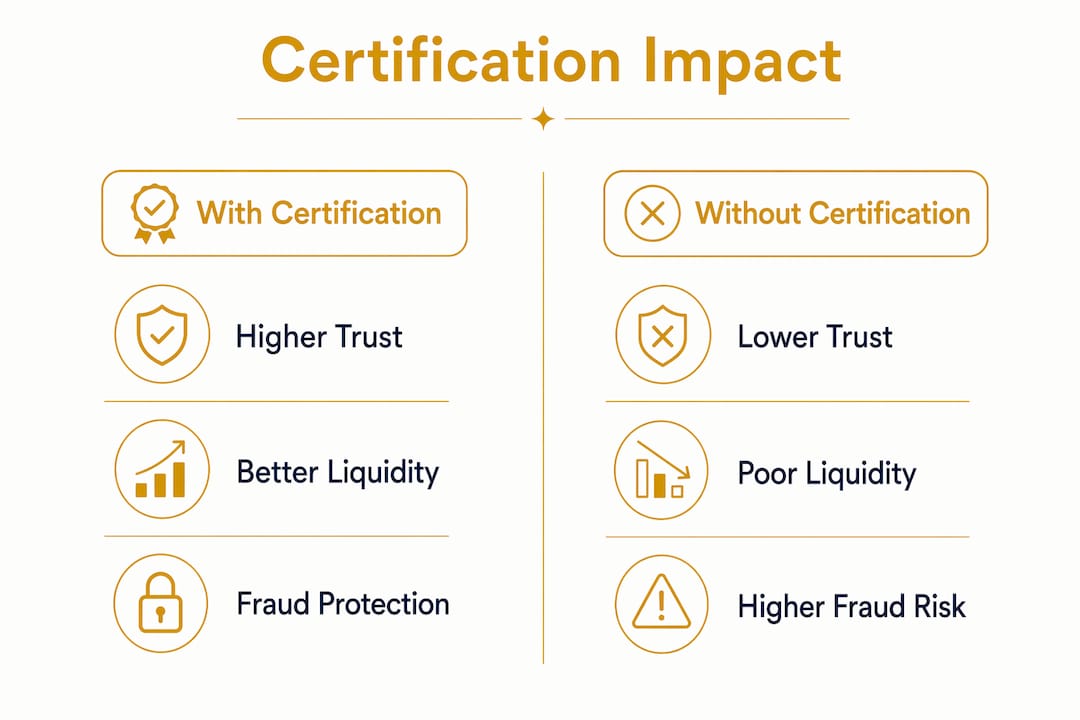

Certification is the single most powerful risk mitigation tool available to gemstone investors, and its absence transforms a potential asset into a speculative gamble. The industry standard is a grading report from a recognized laboratory, with GIA, AGS, and IGI representing the most widely accepted authorities in the United States and internationally.

Certification from recognized labs increases buyer trust and liquidity, and is required to verify authenticity and quality grades. Without a current report, resale becomes difficult and insurance coverage is either unavailable or based on subjective appraisal rather than objective grading. This creates a compounding problem: an uncertified stone is harder to sell, harder to insure, and harder to price accurately.

The financial impact of certification on liquidity is measurable. High-quality certification and pristine condition can shrink buy-sell spreads by 30% or more, which is the difference between a viable investment and one that bleeds value on every transaction. A GIA-certified Burmese ruby with a “no heat” notation commands a premium that an uncertified stone of identical appearance simply cannot access.

| Certification status | Resale ease | Insurance access | Fraud protection | Typical spread |

|---|---|---|---|---|

| Current GIA/AGS/IGI report | High | Full coverage available | Strong | Narrower by up to 30% |

| Expired or outdated report | Moderate | Limited or conditional | Partial | Wider, buyer skepticism |

| No certification | Low | Difficult or unavailable | Minimal | Widest, significant discount |

Counterfeit certificates represent an emerging threat. Sophisticated forgeries of GIA reports circulate in secondary markets, particularly online. Buyers should verify report numbers directly on the GIA Report Check database before completing any transaction.

Pro Tip: For opals specifically, certification requirements differ from faceted stones. Australianopaldirect’s opal certification guide explains what documentation to request and why provenance from named Australian mining regions like Lightning Ridge adds measurable resale value.

What practical factors affect liquidity and resale value?

Liquidity in gemstone investing is conditional, not guaranteed, and the conditions that determine it are specific and often underappreciated by new collectors. Timing, provenance, condition, and market sentiment all govern liquidity, and urgency in selling compresses prices significantly. This is the structural reality that separates gemstone investing from any exchange-traded asset class.

Economic cycles exert direct pressure on the gemstone market. Luxury colored stones and fine jewelry tend to hold value better than discretionary consumer goods during moderate downturns, and luxury jewelry serves as a defensive asset class during inflation and market volatility. However, this defensive quality requires patient, long-term holding. Forced sales during severe contractions still produce discounts, because the buyer pool for a $50,000 alexandrite is narrow regardless of macroeconomic conditions.

Transaction costs deserve careful modeling before any purchase. Auction house buyer’s premiums typically range from 15% to 25% of the hammer price, and seller’s commissions add another layer. Private sales avoid auction fees but require finding a qualified buyer independently, which takes time and network access. These costs mean a gemstone must appreciate meaningfully before the investor breaks even on a round-trip transaction.

- Condition: chips, scratches, or color fading reduce resale value and buyer confidence

- Documentation: provenance records from named origins (Burma, Colombia, Lightning Ridge) add premium

- Storage: climate-controlled, secure storage prevents physical degradation and supports insurance claims

- Portfolio sizing: most financial advisors recommend limiting alternative assets, including gemstones, to 5% to 10% of total portfolio value

- Exit planning: build a 12 to 24 month exit timeline into any gemstone investment thesis

Understanding insurance coverage for valuable gemstones is not optional for serious collectors. A stone that is lost, stolen, or damaged without adequate coverage represents a total loss, and standard homeowner’s policies rarely cover high-value gemstones at replacement cost.

What common pitfalls should investors avoid when buying gemstones?

The most costly gemstone investment mistakes share a common thread: they stem from insufficient due diligence at the point of purchase, when the excitement of acquiring a beautiful stone overrides financial discipline. The following sequence of pitfalls, ordered by frequency and financial impact, gives investors a practical framework for avoiding them.

-

Buying uncertified or misdescribed stones. Purchasing a stone without a current report from GIA, AGS, or IGI is the single most common and most expensive mistake. Buying from trusted dealers with lab reports and provenance documentation significantly reduces fraud risk and enhances investment safety.

-

Overpaying for common stones without rarity. Commercial-grade amethyst, blue topaz, and citrine are produced in large quantities and carry minimal investment premium. Rarity drives collector value; abundance does not. Investors should focus on stones with documented scarcity, specific geographic origins, or exceptional color grades.

-

Ignoring gemstone treatments and their value impact. Heat treatment, fracture filling, and beryllium diffusion are standard practices across the colored stone trade, but they affect value dramatically. A comprehensive understanding of gemstone treatments is required before evaluating any purchase. An untreated Burmese sapphire commands a premium of 30% to 100% over a heat-treated equivalent of the same color, depending on size and quality.

-

Neglecting proper storage and care. Opals require stable humidity to prevent crazing. Emeralds, which are typically fracture-filled with cedar oil or resin, need periodic re-oiling to maintain their appearance. Storing gemstones incorrectly accelerates physical degradation and reduces resale value in ways that are often irreversible.

-

Skipping second opinions on high-value purchases. For any stone above $5,000, an independent appraisal from a Graduate Gemologist (GG) credentialed by GIA provides a critical check on the seller’s description and asking price. The cost of a second opinion is trivial relative to the downside of overpaying.

Key takeaways

Gemstone investment risk is manageable with certification, realistic liquidity planning, and disciplined ownership costs, but it cannot be eliminated by enthusiasm alone.

| Point | Details |

|---|---|

| Certification is non-negotiable | GIA, AGS, or IGI reports reduce fraud risk and can narrow buy-sell spreads by 30% or more. |

| Illiquidity requires long time horizons | Plan for 12 to 24 month exit timelines; forced sales consistently produce significant price discounts. |

| Ownership costs compound against returns | Storage, insurance, and transaction fees must be modeled before purchase, not after. |

| Treatments dramatically affect value | Untreated stones command premiums of 30% to 100% over treated equivalents; always verify treatment status. |

| Rarity and provenance drive resale | Named origins like Lightning Ridge, Burma, and Colombia add measurable, documented premium at resale. |

What I’ve learned about patience and discipline in gemstone investing

After years of observing collectors enter and exit the gemstone market, the pattern that separates successful investors from disappointed ones is not superior taste or access to rare stones. It is the willingness to hold. The investors I have seen lose money on gemstones almost always share one characteristic: they needed to sell before the market was ready to meet their price.

The myth that gemstones are a liquid store of value, like gold bullion, persists because it is emotionally appealing. A stone that carries the fire of Lightning Ridge or the deep blue of a Kashmir sapphire feels like it should command its price on demand. The market does not share that sentiment. Investors often underestimate costs and illiquidity, and the resulting disappointment is not a failure of the asset class. It is a failure of expectation management.

What I find genuinely encouraging is that the collectors who approach gemstones with passion first and investment thesis second tend to fare better. They hold longer because they love what they own. They care for their stones properly because the stones matter to them. And when the market does align with their exit, the combination of pristine condition, current certification, and documented provenance produces outcomes that purely financial buyers rarely achieve. The luxury gemstone standards that protect value are the same standards that make a collection genuinely beautiful to own.

My honest advice: treat gemstone allocation as a long-term commitment, size it conservatively within your portfolio, and never purchase a stone you would not be content to hold for a decade.

— Renee

Discover authenticated Australian opals at Australianopaldirect

Australianopaldirect sources every opal directly from earth-mined operations across Lightning Ridge, Coober Pedy, and Queensland, with direct-miner relationships that eliminate the middlemen who introduce misrepresentation risk. Each piece in the collection carries documented provenance and is backed by complimentary insurance, a 90-day warranty, and free shipping, addressing the ownership cost concerns that erode returns on uncertified stones. For collectors ready to invest with confidence, Australianopaldirect’s expert investment guidance and curated Limited Edition Opals collection offer a starting point grounded in authenticity, transparency, and genuine gemological expertise. Explore the full collection at Australianopaldirect.

FAQ

Is gemstone investment safe compared to stocks and bonds?

Gemstone investment carries higher illiquidity risk, wider transaction costs, and greater fraud exposure than equities or fixed-income assets. It functions best as a long-term, passion-driven allocation rather than a liquid portfolio component.

What labs certify gemstones for investment purposes?

GIA, AGS, and IGI are the most widely recognized grading laboratories for investment-grade gemstones. Reports from these institutions are the minimum standard for resale and insurance in most markets.

How do gemstone treatments affect investment value?

Treatments such as heat enhancement, fracture filling, and beryllium diffusion reduce a stone’s investment premium significantly. Untreated stones with lab-verified natural status command premiums of 30% to 100% over treated equivalents of comparable appearance.

What percentage of a portfolio should gemstones represent?

Most financial advisors recommend limiting alternative assets, including gemstones, to 5% to 10% of total portfolio value. This sizing reflects the illiquidity and long exit timelines inherent to the asset class.

How can investors verify a gemstone certificate is authentic?

Buyers should verify GIA report numbers directly through the GIA Report Check database before completing any transaction. Counterfeit certificates circulate in secondary and online markets, making independent verification a required step in due diligence.

Recommended

- Luxury gemstone standards explained: Expert guide for collectors - Australian Opal Direct

- Expert luxury jewelry investment tips: Sourcing Australian opals - Australian Opal Direct

- Key features of opal investment pieces: a collector’s guide - Australian Opal Direct

- Why Invest in Opals: Rarity, Value, and Ethical Appeal - Australian Opal Direct